Introduction

The fundraising market for private fund sponsors continues to be incredibly competitive. This article explores some of the strategies that sponsors are employing to attract and retain investors.

It will always remain the case that the best ingredients for a successful fundraise are:

- a consistent track record proven over economic cycles;

- a stable investment team; and

- a compelling (and sometimes distinctive) investment thesis which in more recent periods has resulted in more concentrated fund strategies focusing on specific sectors.1

For some fund sponsors those ingredients can often be sufficient to reach a target fundraise without offering additional inducements to investors.

But for many fund sponsors (and particularly in the increasingly competitive fundraising market for private credit) offering inducements to investors is a core part of any fundraising strategy. These can be broadly split into three types of inducements: (i) economic inducements; (ii) ownership inducements; and (iii) non-economic inducements.

Economic inducements

Economics within the private fund industry have come under scrutiny in recent years. The 2% management fee: 20% carried interest model is no longer accepted as the norm but requires justification. This is especially so in a high interest rate environment. As a result, sponsors typically now offer as standard:

- discounts available to many investors on the basis of a defined “rate card” (i.e. widely publicised promotions); and

- discounts available to certain key investors on the basis of a wider relationship (i.e. targeted discounts to particular groups).

Management fee inducements

Discounts available to many investors

Many private fund sponsors (and most private credit sponsors) will establish a tiered rate card for management fee discounts at the start of the fundraising (following market testing), with fee discounts offered to investors based on their:

- “Aggregated commitment”; and/or

- “Date of investment”

An investor’s management fee will be reduced by a certain number of percentage points, determined by a combination of their Aggregated commitment and Date of investment.

Read our article on The evolution of direct lending fund fee structures for further insights on the increasing fluidity in fee structures in private debt funds.

Aggregated commitment discounts

An investor’s Aggregated commitment can combine some or all of the following amounts (and which vary from sponsor to sponsor):

- size of the investor’s commitment;

- size of the commitments of the investor’s associates, or investors managed or advised by the same manager or adviser;

- size of the commitments of investors introduced to the sponsor by the same “gatekeeper” or investment consultant as the investor; and

- size of the investor’s commitment (and its affiliated investors’ commitments referred to above) to one or more prior funds (or other fund strategy managed by the sponsor).

Some sponsors will specify in the fund documentation that an investor’s Aggregated commitment is its commitment when aggregated with such other commitments as the sponsor determines in its discretion. In practice, this is then determined and confirmed in each investor’s side letter on an investor-by-investor basis (and the basis on which commitments can be aggregated excluded from the MFN).

Date of investment discounts

So called “early bird” discounts are often offered to investors by reference to some or all of the following dates (and which vary from sponsor to sponsor):

- first closing date;

- a date falling (x) months following the first closing date; or

- any date prior to the date on which the fund has accepted commitments in excess of (x) million (including any commitments accepted on that date which take the fund over that threshold).

Some sponsors will provide that an investor’s Date of investment reflects the first date on which one of its affiliated investors (described above) makes a commitment to the flagship fund program (rather than the date on which the investor itself makes a commitment).

Other economic inducements

While less common, some sponsors will also offer other economic inducements (similarly subject to Aggregated commitment and Date of investment requirements) providing for (in order of prevalence in our experience):

- a management fee discount or holiday limited to a particular period of time (for instance, during the fundraising period);

- a reduced carried interest rate;

- a waiver of equalisation interest due on equalisation contributions relating to management fee;

- a reduced carried interest catch-up rate;

- an increased preferred return/hurdle; and

- in relation to open-ended funds and evergreen funds, preferential liquidity terms (for instance, reduced redemption charges).

The models below demonstrate the differing impact of a preferred return rate versus to a slower carried interest catch-up model.

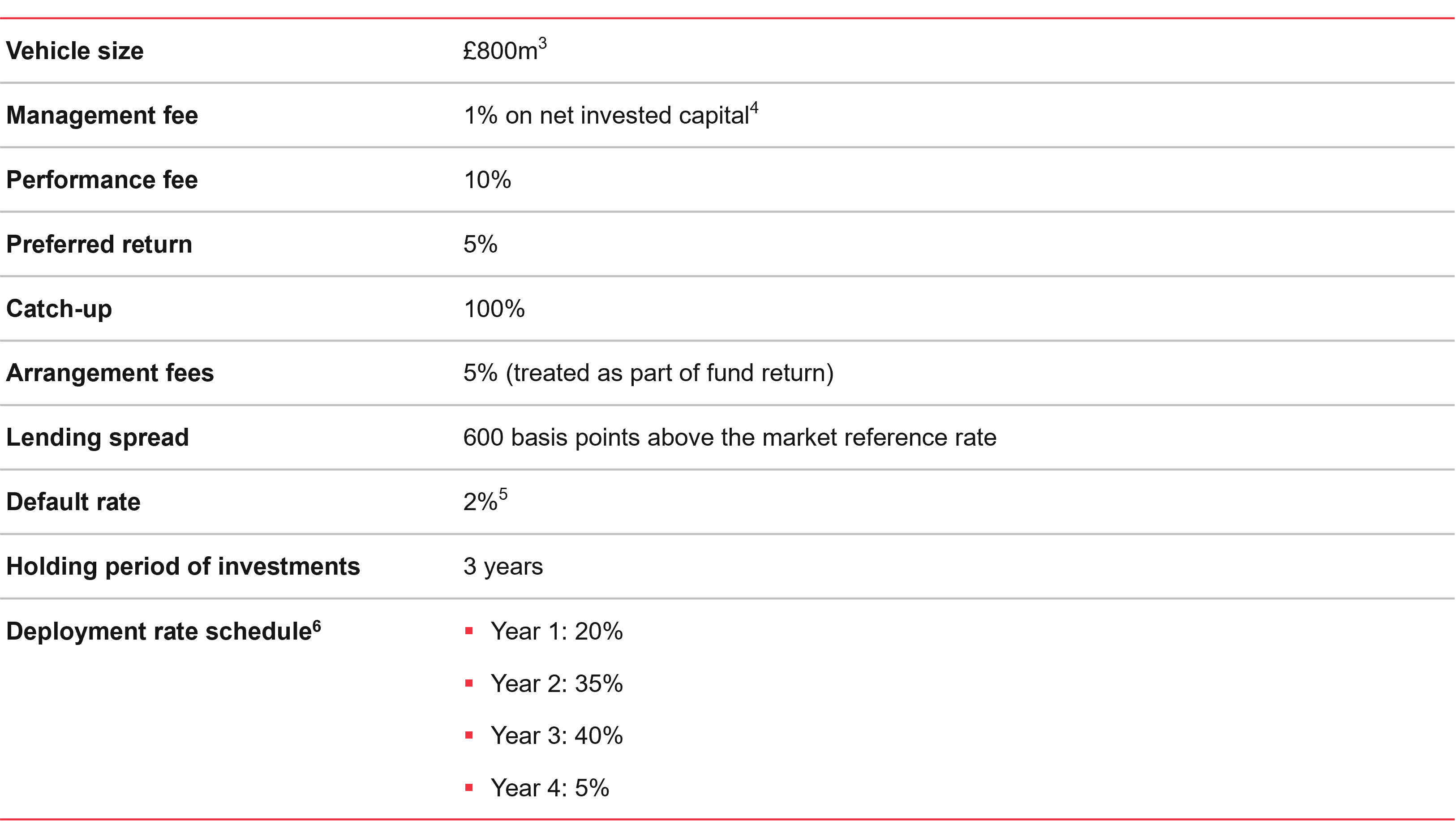

Base case assumptions

In order to compare different potential approaches to fee structures, we first look at the typical fee structure of an unlevered2 closed ended drawdown direct lending fund to establish a base case.

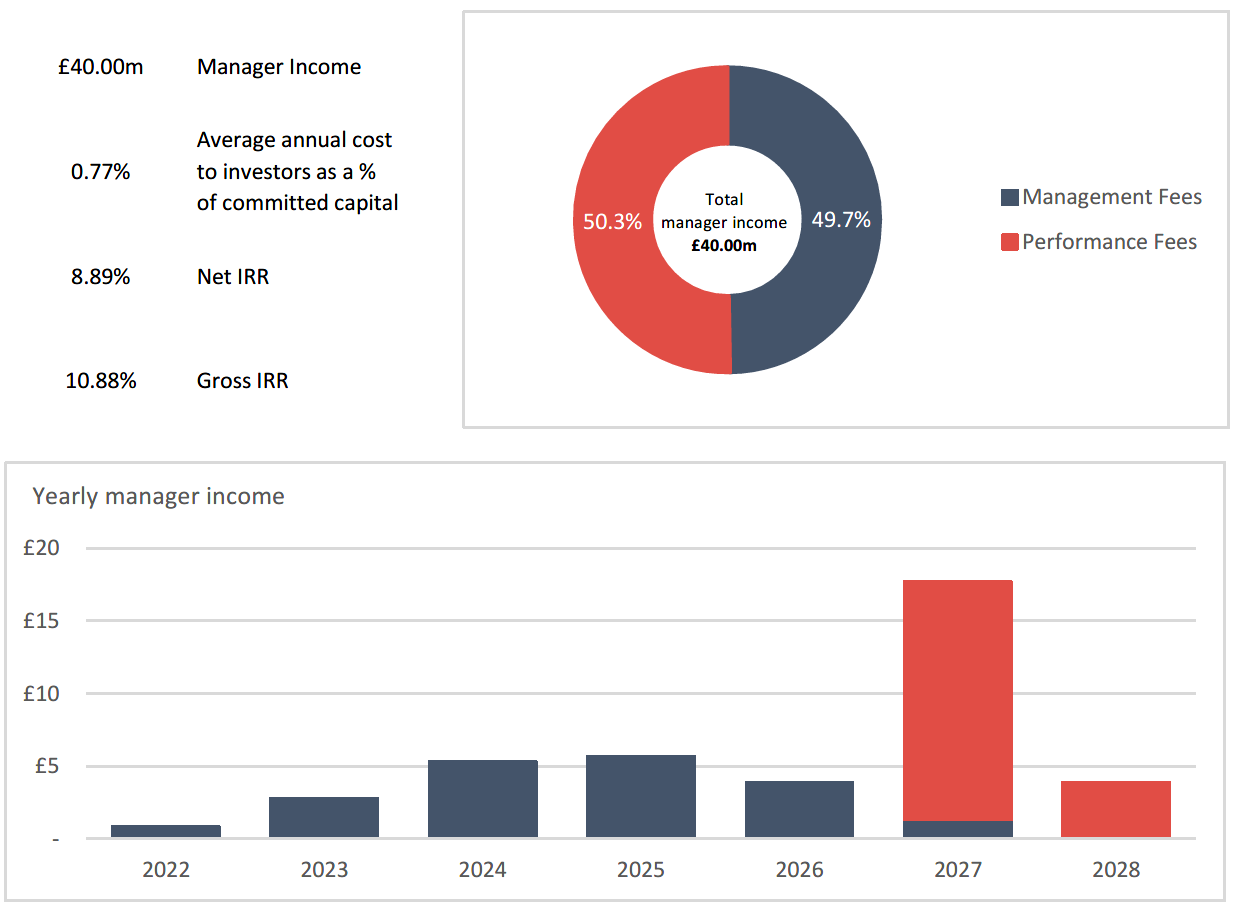

Scenario 1: Base case - no discount; consistent performance

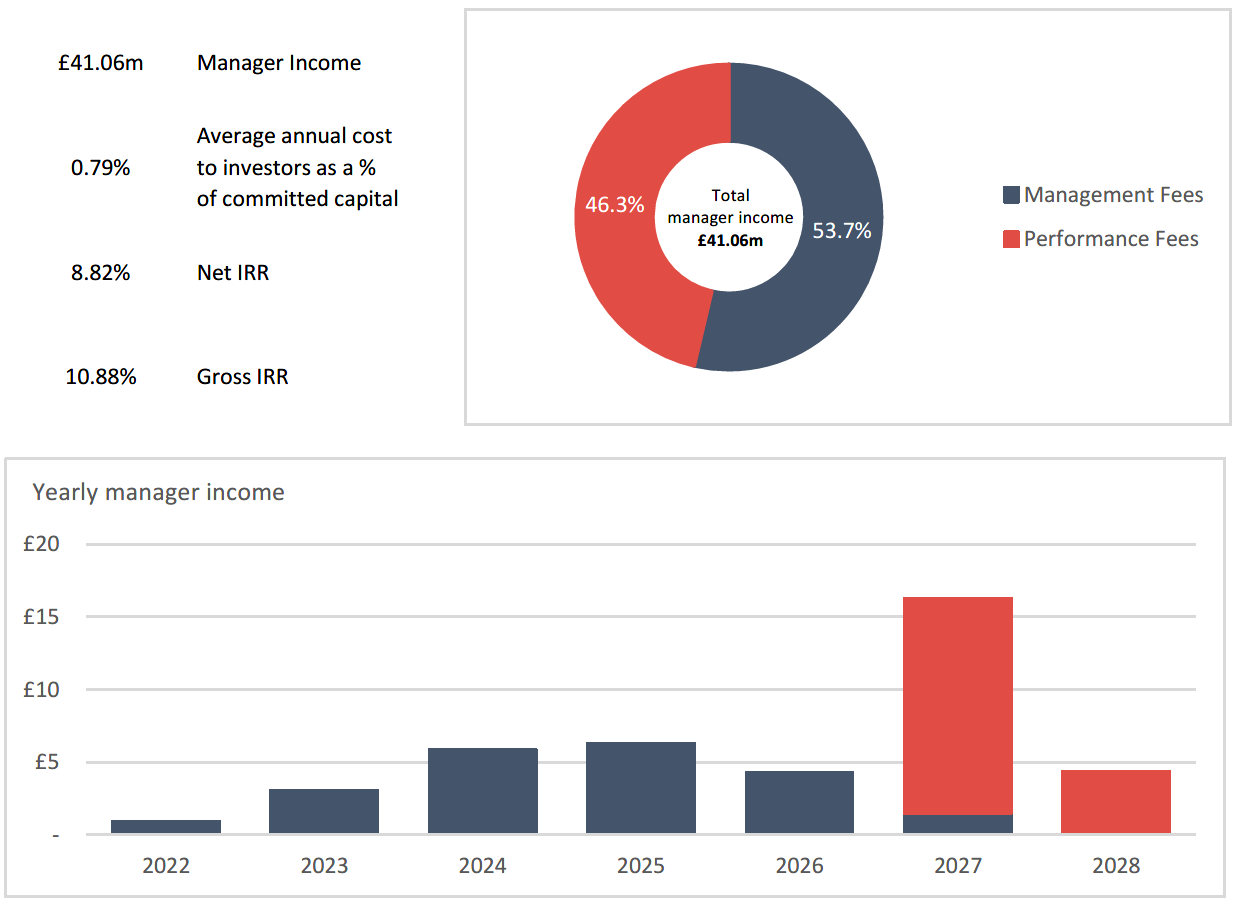

Scenario 2: Management fee discount (0.25% reduction); consistent performance

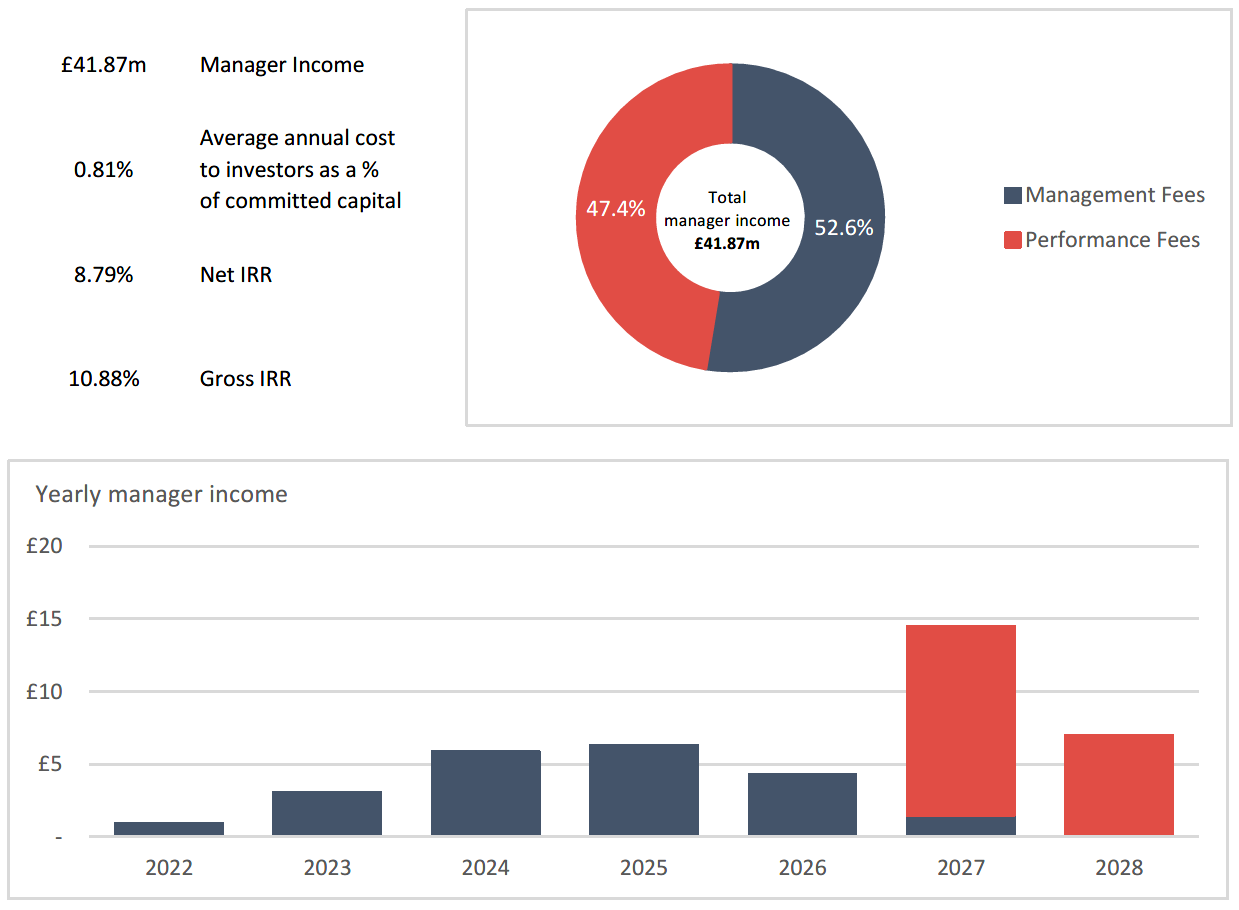

Scenario 3: Carried interest discount (2% reduction); consistent performance

Scenario 4: Lower catch up rate (50%) and preferred return (7%); consistent performance

Some sponsors have also entered the fundraising market offering alternative fee structures to meet the preferences of different investor groups, offering:

- a standard management fee and carried interest rate; alongside

- a lower management fee but higher carried interest rate.

Co-investment

Sponsors will often seek to offer preferential co-investment rights to key investors which, in effect, offer a lower management fee and carried interest rate for an investor on a blended basis (when aggregated with an investor’s investment in the flagship fund program).

In this context, by “co-investment” we are referring to opportunities to invest alongside a flagship fund where that flagship fund is constrained from taking up the entire investment opportunity (rather than separately managed account (SMA) arrangements where SMAs co-invest alongside a flagship fund in all investments by reference to an allocation policy).

Preferential co-investment rights can take several forms, including:

- non-contractual, relationship driven, priority allocations of co-investment opportunities with key investors that have the ability to transact quickly on co-investment transactions (which is more common in private equity);

- a confirmation in the side letter that, to the extent offered to an investor, a certain amount (e.g. an amount equal to an investor’s commitment to the flagship fund program) of co-investment opportunities will be offered to an investor on a “fee free” basis;

- priority allocations agreed in side letters providing for co-investment opportunities to be allocated between key investors (often allocated pro rata to the commitments of those key investors who elect to participate in a particular co-investment opportunity);

- a dedicated “top-up fund” raised alongside the relevant flagship fund, with key investors having priority to make commitments to such a “top-up fund” which then co-invests alongside the flagship fund on a discretionary basis (typically with lower or no management fee and carried interest); and

- dedicated co-investment SMAs raised alongside the flagship fund to provide key investors priority access to co-investments alongside that flagship fund (whether on a discretionary or non-discretionary basis).

GP stakes and ownership inducements

Indirect fundraising benefits

Historically, the relationship between GP stake transactions and fundraising has often been indirect. This results from the fact that traditional GP stakes funds will normally only look to acquire minority stakes in the sponsor itself, without making a commitment to funds managed by that sponsor.

Nevertheless, having a GP stake investor may still provide certain indirect benefits to a sponsor in terms of its future fundraising. For example:

- there may be reputational benefits, with an investment by a well-known GP stakes investor seen as stamp of approval which in turn gives investors increased confidence in the sponsor;

- the proceeds from a stake sale can be used by the sponsor to grow its business, for example by funding increased GP commitments in a manner that achieves increased alignment with investors, or by funding working capital for new initiatives such as geographical expansion or team hires, all of which may ultimately increase AUM; and

- the GP stake investor is often a strategic partner to the sponsor rather than just a passive owner, and many GP stake investors will emphasise their ability to assist with capital formation by facilitating introductions to investors.

Direct fundraising benefits

As the GP stakes market has grown and matured, we have seen an increase in hybrid models where a GP stake investment in a sponsor is directly linked to investor commitments to funds managed by that sponsor.

These hybrid models often involve innovative structuring, such as equity warrants under which the GP stake investor has the option to increase its percentage ownership stake in the sponsor if it meets certain monetary thresholds in respect of capital commitments to funds managed by that sponsor.

We also see variations on this model where the equity warrants were not linked solely to capital commitments by the relevant GP stake investor. Instead, they are linked to investments made by any investors located in the same geography, on the basis that the sponsor’s association with that investor creates a halo effect which would assist with raising capital in that region.

A factor contributing to the rise of these hybrid models is the increasingly prevalence of secondary trades by GP stake investors, where the syndication of part of an existing investor’s stake in the sponsor may be linked to the purchaser also making capital commitments to funds managed by the sponsor.

Another factor is the increasing range of players in the market outside of the traditional GP-stakes funds. For example, investor surveys have shown that sovereign wealth funds, who have previously invested into GP stakes funds, are increasingly considering going direct and taking their own stake in an underlying sponsor, particularly where they may already be an investor in funds managed by that sponsor. Private wealth and family offices are also prevalent in this area - acquiring stakes in sponsors alongside making commitments to their funds. That is in part driven by the wider convergence of private wealth and private capital, with hybrid investments in sponsors and their funds providing an appealing way for private wealth to increase exposure to private markets but without taking single-company risk. In addition, the ability of private wealth to provide patient capital fits well with the nature of GP stake investing, particularly for emerging sponsors.

The growing market, the wider range of players in that market and the increasingly prevalence of hybrid models all provide opportunities for sponsors to actively seek to link GP stake transactions with commitments to their funds.

Revenue-share arrangements

Another trend we are seeing is the increased use of revenue-share arrangements as an inducement to fundraising. These arrangements involve an investor seeding a fund in return for receiving a revenue share from the sponsor equal to a percentage of all of the management fees and carry of the whole fund.

From an investor’s perspective, this can provide more upside than would be achieved through a management fee waiver, as a management fee waiver is capped at the investor’s own management fees whereas the revenue-share operates on a whole fund basis with unlimited upside.

From a sponsor’s perspective, a revenue-share arrangement can be an appealing form of ownership inducement without constituting a full GP stake transaction in the traditional sense, as it only gives away economics in respect of a single fund rather than granting the investor a share of economics referable to future funds. In addition, legally documenting a revenue-share arrangement is easier to implement than a traditional GP stake transaction.

Non-economic inducements

Investors’ non-economic requirements have continued to become more complex over time.

Being able to accommodate a particular investor’s legal, regulatory, tax, ESG and reporting requirements (whether via a side letter or a bespoke SMA) can be key in attracting and retaining investors.

While the more usual non-economic inducements (advisory committee seats, information rights and additional reporting) are well understood, some of the more novel inducements recently offered by certain sponsors include:

- access to sponsor investment teams through regular meetings;

- reciprocal sharing of secondees and offering training to an investor’s investment team;

- participation in an investor’s annual survey programme and presenting at an investor’s AGM; and

- in relation to open-ended funds and evergreen funds, preferential liquidity terms (for instance, shorter lock up periods).

Most favoured nation issues

When a sponsor is considering offering any form of inducement, it will be important to ensure it considers the impact of any most favoured nation (MFN) provisions.

Investors will expect that, at a minimum, they receive the same economic terms (and often non-economic terms) as other investors who have made the same commitment to a particular vintage of a strategy.

Fund sponsors will often try to distinguish the economic terms that are offered to investors based on: (i) Date of investment; (ii) wider relationships with particular investors; and (iii) perceived negotiating strength of particular investors.

When offering preferential economic terms (and, in some cases, non-economic terms) fund sponsors need to take huge care in ensuring that, regardless of the legal terms of the MFN provisions, an investor does not, without justification, receive better terms than an equivalent investor.

In a private credit fund context, MFN provisions are more complicated where a fund sponsor establishes a number of SMAs alongside the flagship fund. Typically, fund sponsors will try to exclude terms agreed in an SMA from being subject to the MFN provisions of the flagship fund and any other SMAs raised alongside the flagship fundraise.

While separating SMAs from the MFN provisions of other vehicles in the same vintage is common market practice, sponsors must ensure there is some level of transparency around preferential economic terms offered to SMA investors to maintain trust. This is especially applicable given they are ultimately all gaining exposure to the same underlying investment.

Conclusion

Taking a strategic approach to inducements, whether economic inducements, non-economic inducements or ownership inducements, is an important aspect of any successful fundraise.

Fund sponsors would be well advised to establish, at the outset of a fundraise, the various inducements to be offered to investors, ensuring a robust MFN that allows for a tailored approach to inducements and considering the nexus between any GP stake transactions and fundraising efforts. The advice of placement agents and market testing with key investors and investment consultants is crucial to ensure that a sponsor can commit to a consistent and transparent offering during a fundraise.

- Sector-focused fund strategies reflect private capital's evolution towards specialised expertise that can navigate industry-specific risks and opportunities - from regulatory complexities in professional services to supply chain vulnerabilities in manufacturing sectors exposed to tariff uncertainty. This specialisation enables sponsors to develop differentiated transaction execution capabilities and attract investors seeking better exposure to specific market segments with compelling risk-return characteristics. See How private capital can thrive amidst tariff uncertainty for more details.

- To simplify our analysis, in the context of assessing private credit fee structures, we focus on private credit structures for unlevered vehicles, but a similar analysis can also be performed for levered vehicles.

- For simplicity, we are assuming a GBP denominated fund. A similar analysis can be performed for a multi-currency direct lending fund.

- The average management fee seen within direct lending will likely be slightly lower than 1% once factoring in negotiated discounts for early or large commitments. 1% has been used as a simplifying assumption for this analysis.

- This default rate is broadly in line with the Proskauer’s Private Credit Default Index. Overall default rates have fluctuated around 1.4-2.7% between Q3 2022 and Q2 2024.

- Investments are spread evenly over the quarters for each year. Additional assumptions for a buffer and working capital have been made.