Different models of evergreen fund are seen in the market, spanning from NAV-based open-ended structures to hybrid/vintage vehicles that combine elements of closed and open-ended funds1. Where sponsors opt for NAV-based structures, we see a range of approaches adopted relating to investor subscriptions and redemptions, as sponsors grapple with the challenges of marrying investor demand for deployment and liquidity with portfolio construction.

This note considers some of the principal subscriptions models used by sponsors who adopt a “commitment/drawdown” approach2. We will focus on redemptions in a separate note.

Picking the right model

The evolution of different models has been driven by sponsor needs to balance investors’ desire for certainty of deployment against operational complexity and equitable treatment of investors.

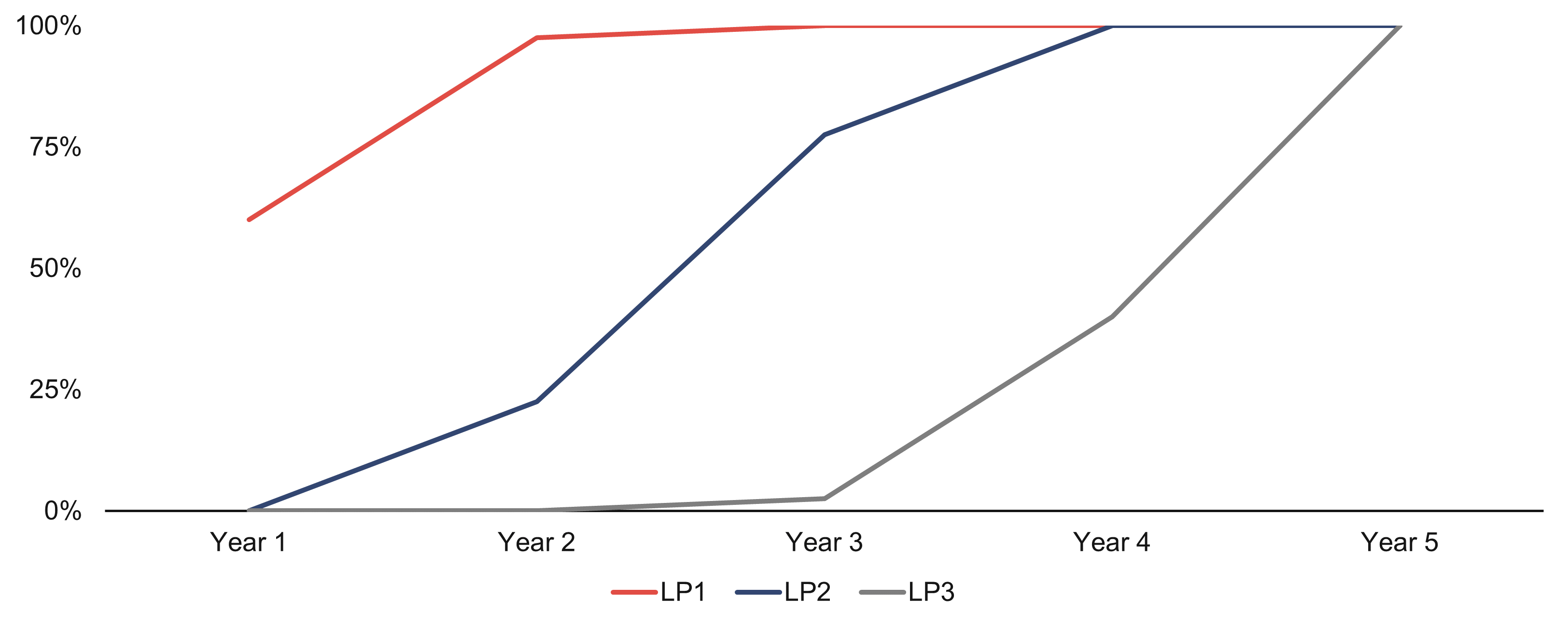

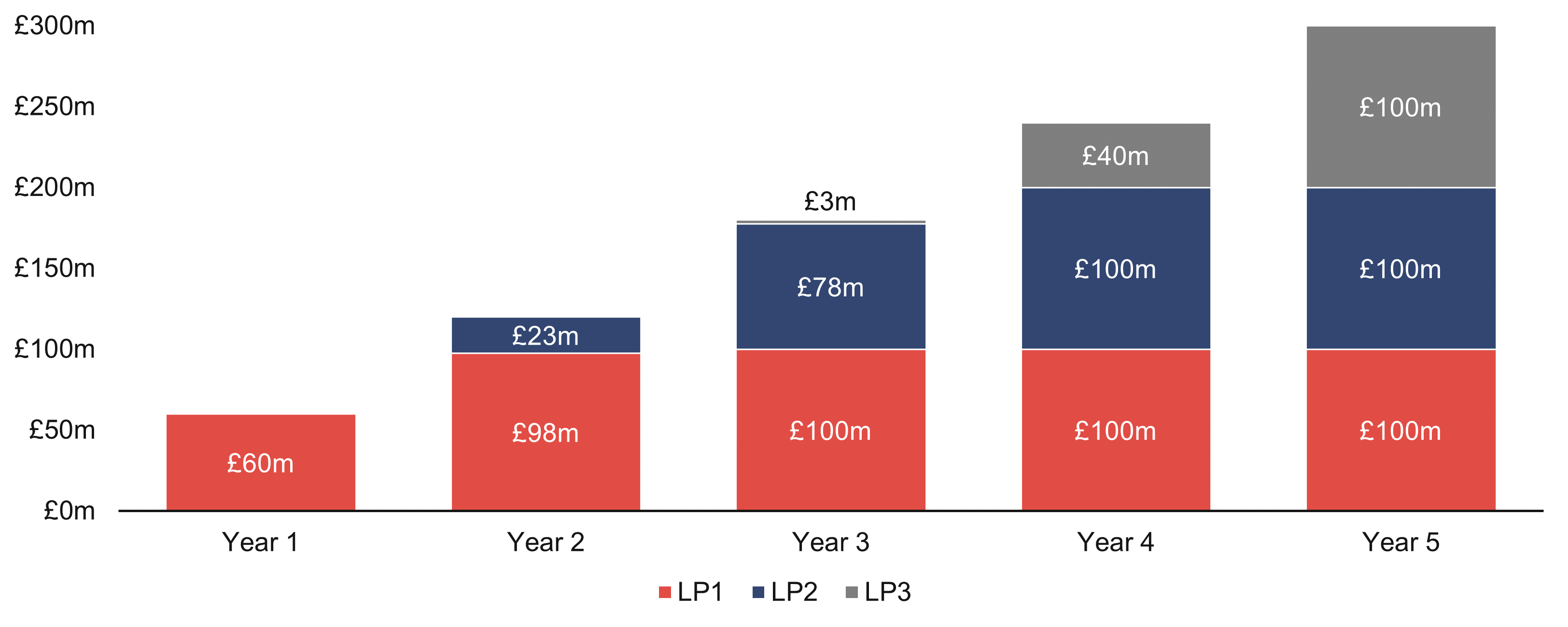

1. First in model

Under this model, commitments are drawn on a first-come, first-served basis. This ensures early close investors are prioritised, which can incentivise prompt commitment and increases investor certainty of full deployment. However, this can result in later investors waiting a considerable time before their capital is called, which can be unattractive and potentially dissuade them from committing.

To continue to attract subsequent close investors and provide comfort over deployment timeframes, sponsors can negotiate a long-stop date by which commitments must be called, after which undrawn commitments can be cancelled. Provisions of this kind are usually negotiated bilaterally with investors, rather than being standard terms, as sponsors typically prefer to retain flexibility given the inherent uncertainty over deployment timeframes.

First in model deployment speed (cumulative % of capital called)

First in model cumulative capital called per LP

Note: Modelled assuming three investors, each committing £100m. Specifically, investor one subscribes in the first year, investor two in the second and investor three in the third. Additionally, annual investment pace is £60m, allocated among investors based on their subscription timing and the scenario applied.

Source: Macfarlanes.

2. Gated first in model

As with the “first in model”, this model provides priority to early close investors, but only up to a guaranteed percentage of their subscription (e.g. 75% of their subscription). Until the early close investors have been called for this guaranteed portion, commitments cannot be drawn from later investors. This model seeks to balance the interests of early and later close investors, although the risk remains that earlier close investors may never be fully drawn down, if the fund receives significant future commitments.

Gated first in model deployment speed (cumulative % of capital called)

Gated first in model cumulative capital called per LP

Note: Modelled assuming three investors, each committing £100m. Specifically, investor one subscribes in the first year, investor two in the second and investor three in the third. Additionally, annual investment pace is £60m, allocated among investors based on their subscription timing and the scenario applied.

Source: Macfarlanes.

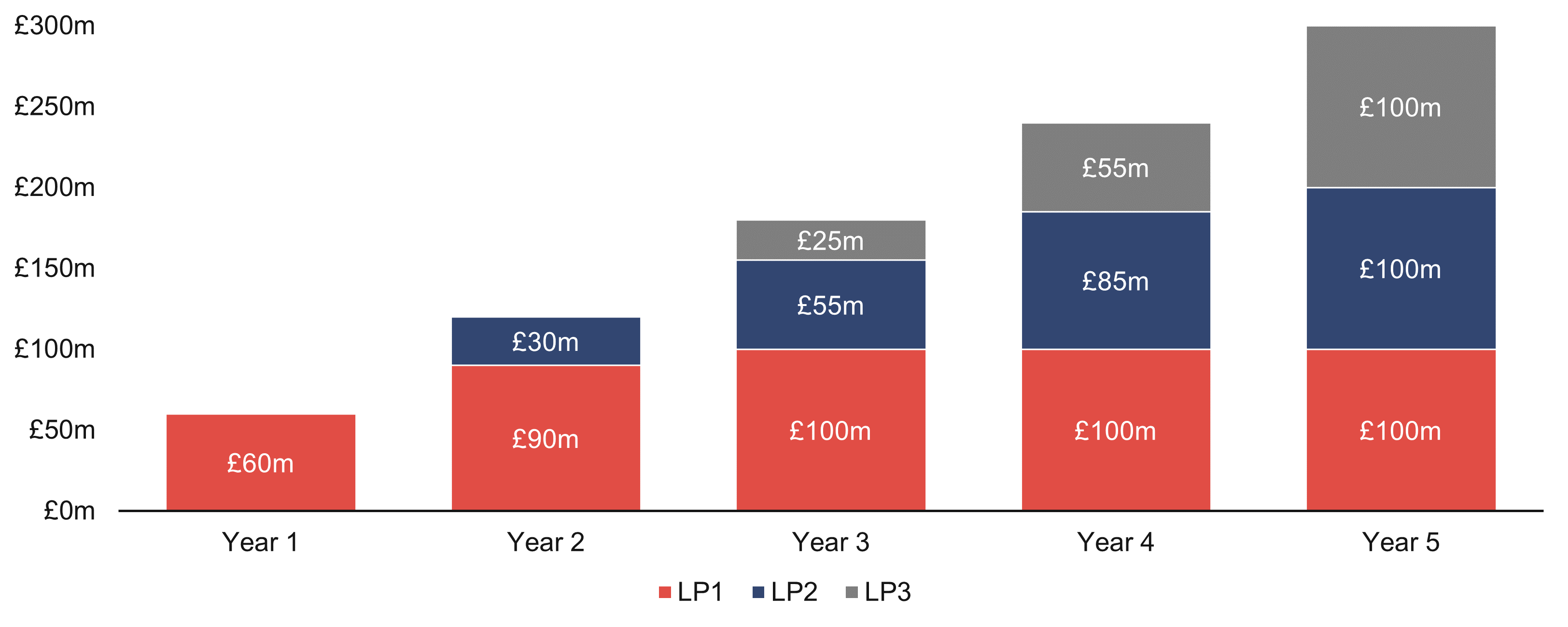

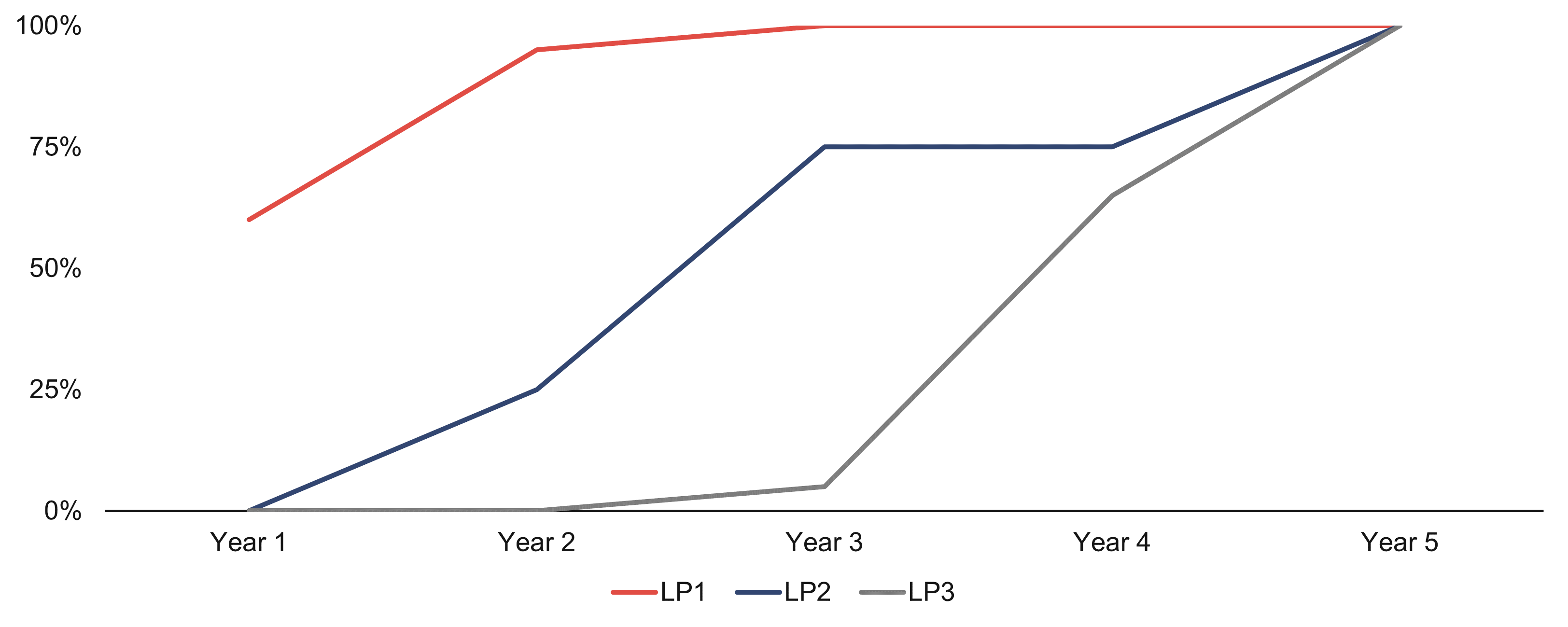

3. Pro rata model

This model sees all investors drawn down pro rata to their undrawn commitments, regardless of when they joined the fund. This approach treats all investors equally but can frustrate early investors, as they receive no benefit for committing early. Operationally, it also means drawing down ever smaller amounts from earlier investors as their undrawn commitments become proportionately smaller over time. Further, if new subscriptions continue to flow in, there is again the risk that early commitments may never be fully drawn.

Pro rata model deployment speed (cumulative % of capital called)

Pro rata model cumulative capital called per LP

Note: Modelled assuming three investors, each committing £100m. Specifically, investor one subscribes in the first year, investor two in the second and investor three in the third. Additionally, annual investment pace is £60m, allocated among investors based on their subscription timing and the scenario applied.

Source: Macfarlanes.

4. Pro rata tranche model

Under this model, all investors are initially drawn pro rata to undrawn commitments. However, once an investor is, for example, 66.6% drawn or has not been fully drawn within a set period (e.g. 12 months), they are moved into a priority queue. This ensures that all investors are eventually fully drawn, with those waiting longest given priority.

Some funds take this model further by introducing an “enhanced priority queue” for investors who remain undrawn after an additional period or threshold, ensuring early close investors are fully drawn ahead of later investors.

Pro rata tranche model deployment speed (cumulative % of capital called)

Pro rata tranche model cumulative capital called per LP

Note: Modelled assuming three investors, each committing £100m. Specifically, investor one subscribes in the first year, investor two in the second and investor three in the third. Additionally, annual investment pace is £60m, allocated among investors based on their subscription timing and the scenario applied.

Source: Macfarlanes.

5. Pro rata discretionary model

This model sees drawdowns generally made pro rata to undrawn commitments, but with the sponsor retaining discretion to vary the process as it deems equitable. This offers maximum flexibility – and is often a sponsor’s preferred option – but places significant responsibility on the sponsor, whose decisions may be scrutinised, especially in volatile markets or during periods of high redemption activity. Investors may also have concerns over the lack of certainty inherent in this model.

Additional considerations

Other factors that can influence the choice of model include:

Availability of warehoused assets

If there are warehoused assets available that have been earmarked for the fund, this can alleviate possible early close investor concerns that their capital will not be deployed quickly enough. This can also benefit the sponsor from a fee calculation perspective. Read our note on direct lending fee structures for more information.

Lock-in period

Investors’ commitments are usually locked-in for a period of two to three years, commencing from the date of the investor’s commitment. During this period, investors are generally unable to exercise any withdrawal, redemption or “run-off election” rights (as applicable). Importantly, undrawn commitments do not automatically expire at the end of the lock-in unless the investor actively exercises such rights.

Use of undrawn commitments for redemptions

Sponsors often reserve the right to use undrawn commitments to meet redemption requests. This can accelerate the deployment of new subscriptions and avoid the need to redirect distributions to fund redemptions, thereby maintaining the fund’s investment momentum.

Recycling of capital

A common key feature of evergreen funds is that they permit recycling of capital, meaning that proceeds from realised investments can be redeployed into new investments. The interest or capital arising from investments will sit in the fund until reinvested. In some instances, sponsors seek to build in the flexibility to distribute the recycled amounts and then recall it as a “re-advance”. In such circumstances, sponsors need to think about the interaction between calling such re-advanced capital and drawing down fresh capital from new subscriptions. If a fund operates a priority queue system, the re-advanced capital is typically not given the same priority as new subscriptions. For example, re-advanced commitments may not enter the initial or enhanced priority queues (as described in the “Pro rata tranche model”), which are reserved for new capital deployment.

Conclusion

The choice of subscription drawdown model in an institutional evergreen fund is a critical structural decision, affecting investor experience, fund operations and the sponsor’s ability to deploy capital efficiently. It is driven by numerous factors and we are seeing different geographical approaches with US funds preferring the “Gated first in model” and European funds preferring the “Pro rata model” (or variants of it).

- For an exploration of some of the different models, read our earlier note on Evergreen credit funds.

- As opposed to the approach of fully funding a subscription on day one.