This is the first article in our two-part series examining private equity (PE) investment opportunities in the education sector. In part one, we explore the market landscape, insights across key verticals, and investment patterns that define the sector. In part two, we examine strategic pathways for value creation, transaction execution considerations, and emerging trends shaping the sector's future.

Introduction

The education sector represents one of the world's largest essential service industries, spanning traditional academic institutions through corporate training and specialised learning platforms, that is estimated to reach $8tn in value by 20301. What distinguishes education from other service sectors is its dual nature as both economic driver and social infrastructure, generating direct returns whilst creating broader economic value through human capital development.

The sector's pandemic-driven digitalisation created unprecedented investment opportunities, with PE activity surging from 42 deals in 2020 to 110 deals in 2021 before normalising to 40 deals by 2024.2 This evolution suggests the market has moved beyond speculative growth toward more disciplined, outcome-focused investment approaches.

For private capital investors, education offers exposure to technology-enabled essential services with defensive characteristics and substantial consolidation opportunities. The sector's structural resilience is particularly notable in the current trade environment, where education exhibits strong tariff insulation due to its service-based delivery model and minimal dependency on physical goods crossing borders (see our tariffs report).

To understand education's growing investment appeal, we will examine its economic fundamentals, geographic opportunity distribution, and evolving deal dynamics.

Why education?

Education’s investment appeal stems from its fundamental role as economic infrastructure. The global education market is projected to expand from $6tn in 2022 to $8tn by 20303, representing a compound annual growth rate (CAGR) of 3.7%, a trajectory that reflects sustained market expansion despite economic uncertainties.

Recent academic research shows that education expenditure significantly influences GDP per capita, with a 1% increase in education expenditure corresponding to a 21.3% increase in GDP, a statistically significant relationship, according to the research, that validates education's substantial economic multiplier effects.4

Education's role in human capital development creates sustainable competitive advantages that transcend economic cycles. Research shows that each extra year of schooling leads to an approximately 9% annual increase in a person’s earnings,and the associated human capital generates positive externalities and spillover effects that benefit entire economies through enhanced productivity and innovation.5 The sector’s inelastic demand also provides defensive investment qualities particularly valuable during periods of economic uncertainty.

Public sector funding constraints present significant opportunities for private capital to drive technology-enabled solutions that address growing skills gaps6 whilst delivering more scalable, cost-effective, and interactive educational experiences. Unlike public institutions constrained by budget cycles and procurement processes, private capital can move quickly to implement technological solutions and respond to evolving market needs.7

However, realising these opportunities requires detailed understanding of both the sector's economics and deal dynamics. Educational investments demand longer time horizons, relationship-focused approaches, and regulatory expertise that differ significantly from traditional PE sectors.

In the next section, we examine 386 PE and real estate transactions in education from 2020-2025, representing £8bn in disclosed investment value across EU and North American markets,8 to reveal key patterns in geographic distribution, performance, and deal dynamics in this evolving sector.

Geographic distribution

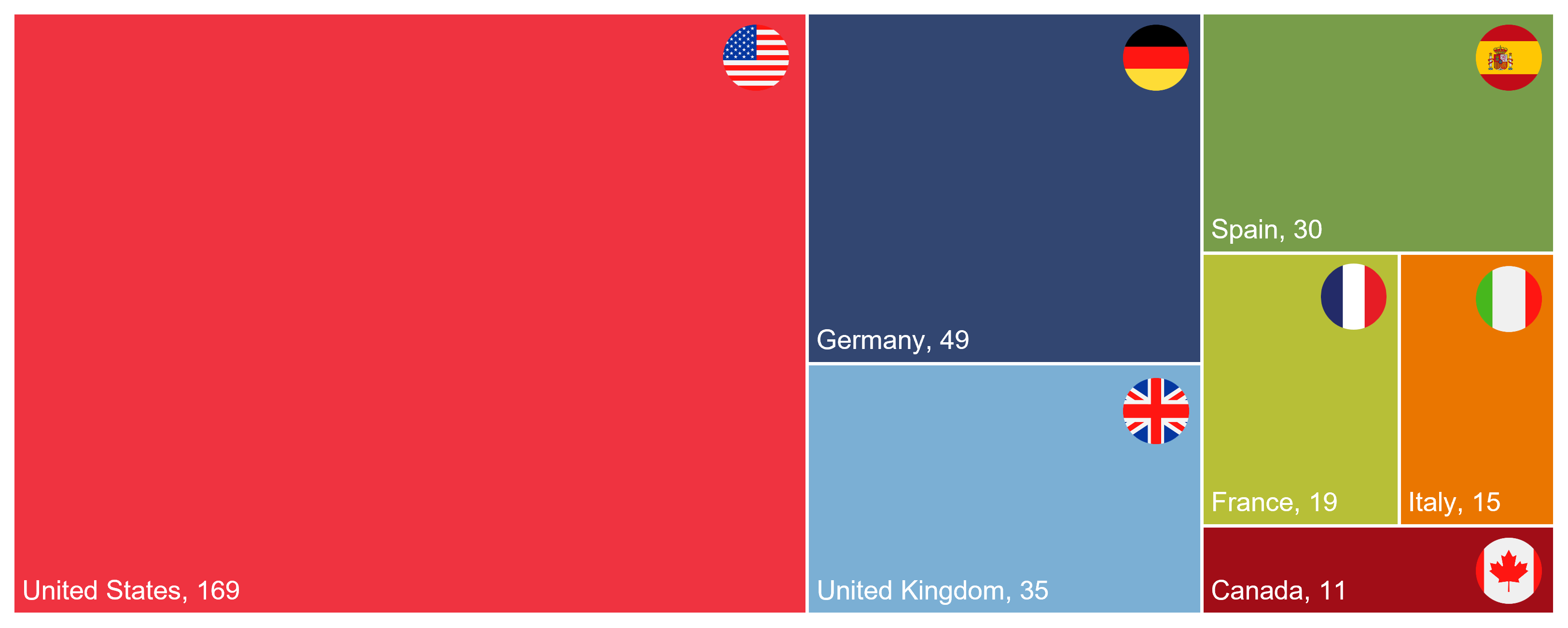

Geographically, North American markets have proven dominant, led by the United States which accounted for 169 deals, representing 43.8% of total transaction volume. When combined with Canada's 11 deals (2.8%), North America represented 46.6% of all education sector PE activity.9 This concentration reflects several structural advantages: mature regulatory frameworks that provide clarity for investors, high per-capita education spending that supports premium pricing models, and established technology ecosystems that facilitate global scaling.

Figure 1: Education deal volume by country

Whilst North America has shown clear scale advantages, Europe presents a more fragmented but collectively significant investment landscape. Germany has emerged as the dominant European market when combining PE and real estate activity in education, totalling 49 deals (12.7%) and positioning it as the second-largest global market behind the US.10 The United Kingdom follows with 35 deals (9.1%), whilst Spain has seen 30 deals (7.8%), positioning it as the fourth-largest global market by transaction count. France and Italy complete the top European markets with 19 deals (4.9%) and 15 deals (3.9%) respectively.11

This distribution across Europe reveals key investment patterns, with Germany's market leadership driven by substantial real estate activity (26 RE deals alongside 23 PE deals) demonstrating institutional appetite for education infrastructure investments.12 The pattern indicates that Northern European markets like Germany show substantial appetite for both education real estate infrastructure and technology investments, reflecting mature capital market development, whilst Southern European markets like Spain have largely focused on education technology modernisation as they accelerate digital transformation of traditional educational systems.

Investment volume analysis

Beyond geographic patterns, the timeline of investment activity reveals equally significant insights about market evolution and capital deployment dynamics.

Figure 2: Deal volume and value, 2020-2025

Note: PE refers to private equity and RE refers to real estate.

Source: Macfarlanes analysis; Preqin, Bloomberg; Data to 31 July 2025.

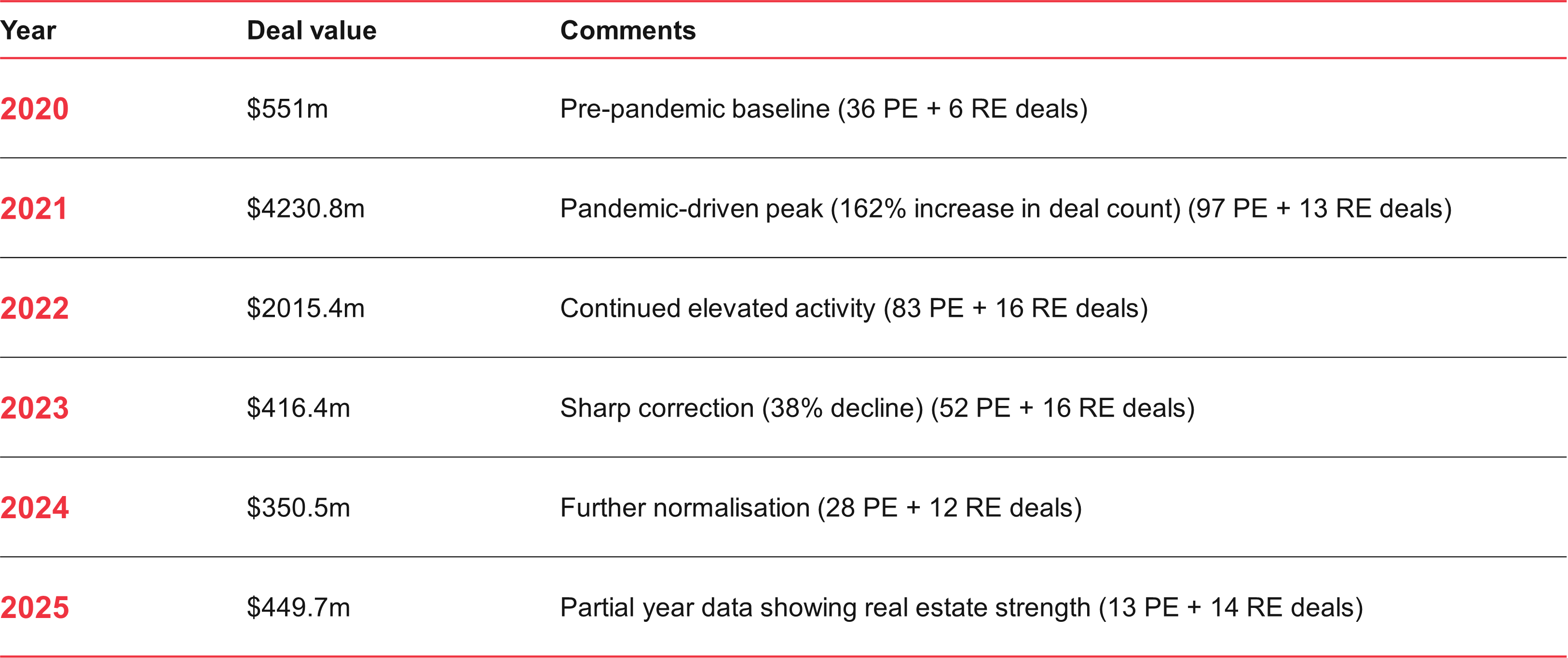

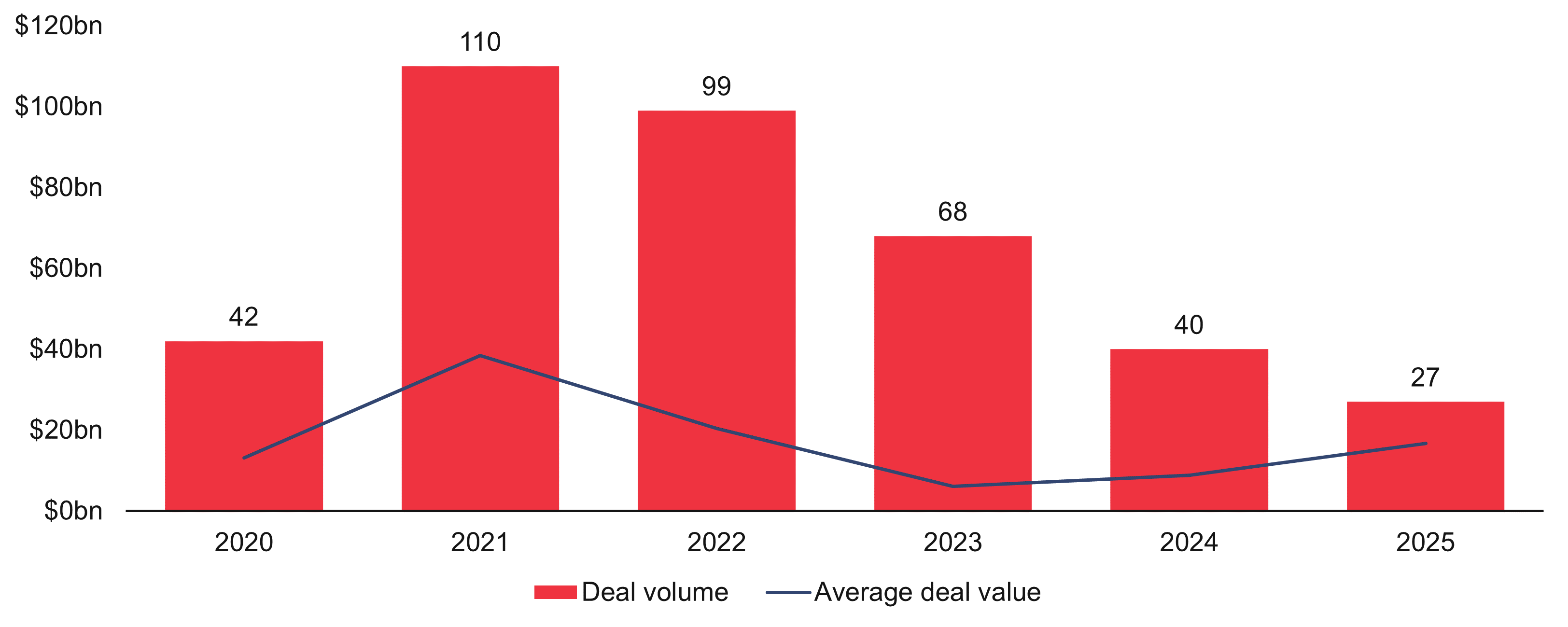

The education sector experienced significant volatility between 2020-2025, as shown in Figure 2, with deal volume surging from a pre-pandemic baseline of 42 private transactions worth $551m in 2020 to a peak of 110 deals valued at $4.2bn in 2021 – representing a 162% increase in transaction count and a nearly eight-fold expansion in total investment value.

This 2021 surge reflects accelerated digitalisation as educational institutions rapidly adopted new technologies during pandemic-driven remote learning requirements. However, the subsequent market correction has been equally pronounced, with deal volume declining to 68 transactions worth $416.4m in 2023 and further contracting to just 40 deals totalling $350.5m in 2024. Deal values thus far in 2025 (worth $449.7m) may suggest a potential rebound in deal activity over Q3 and Q4.

Nonetheless, the parallel decline in average deal sizes – from a peak of $38.4m in 2021 to $8.8m in 2024 as shown in Figure 3 – represents a 76% contraction that signals fundamental shifts in investor behaviour.13

Figure 3: Education deal volume and average deal value, 2020-2025

Source: Macfarlanes analysis; Preqin, Bloomberg; Data to 31 July 2025.

This compression suggests the market has moved beyond speculative investment towards more disciplined approaches, with increased competition for quality assets driving a focus toward earlier-stage investments rather than large-scale acquisitions. The trend could suggest investors are prioritising proven business models and sustainable growth over the more experimental digital learning platforms that dominated pandemic-era dealmaking.

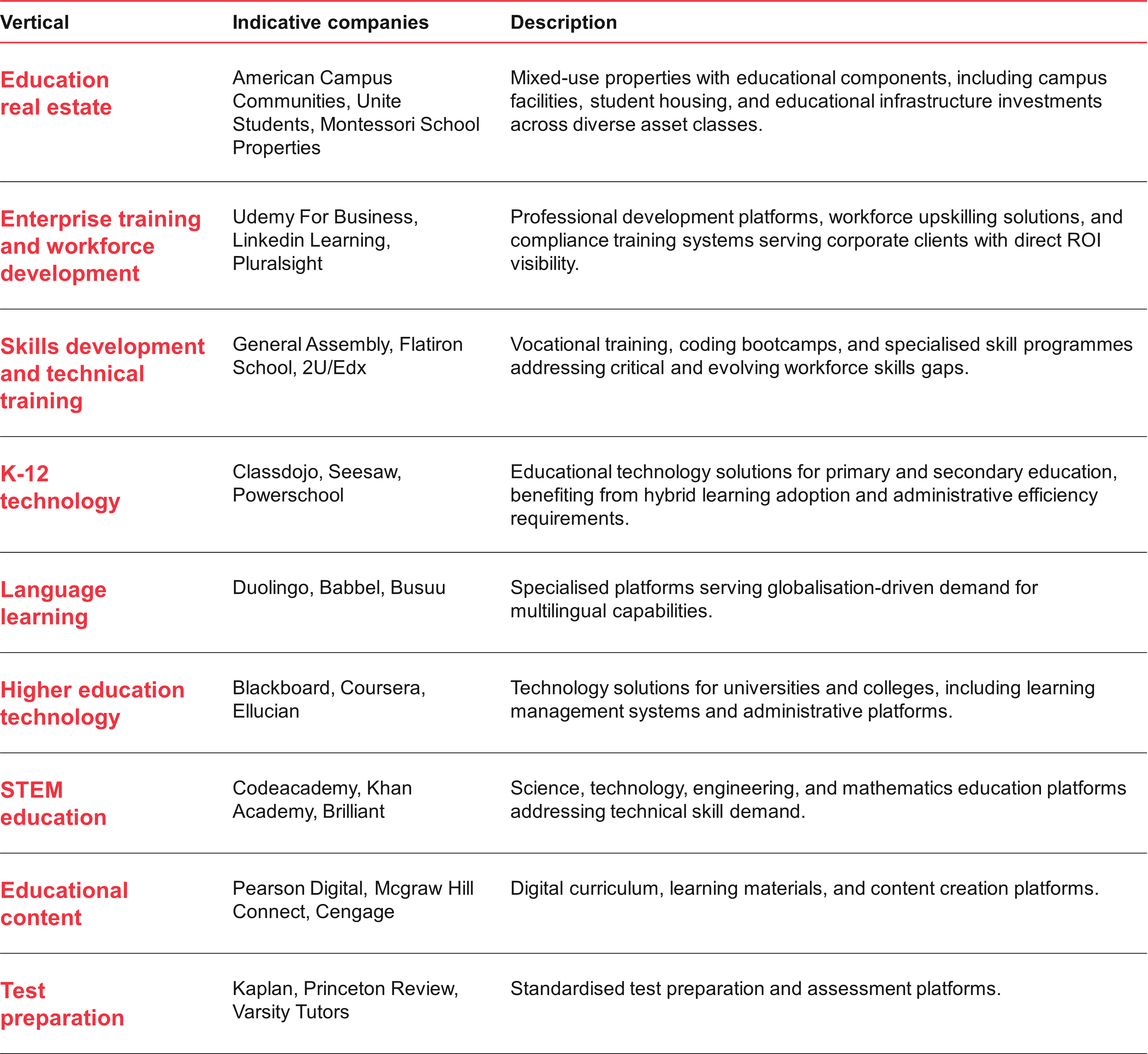

Key education verticals

Understanding where private capital flows across different education segments provides crucial insights for strategic positioning, as noted in Figure 4 below.

Figure 4: Deal activity by education vertical, 2020-2025

Emergence of education real estate and corporate training

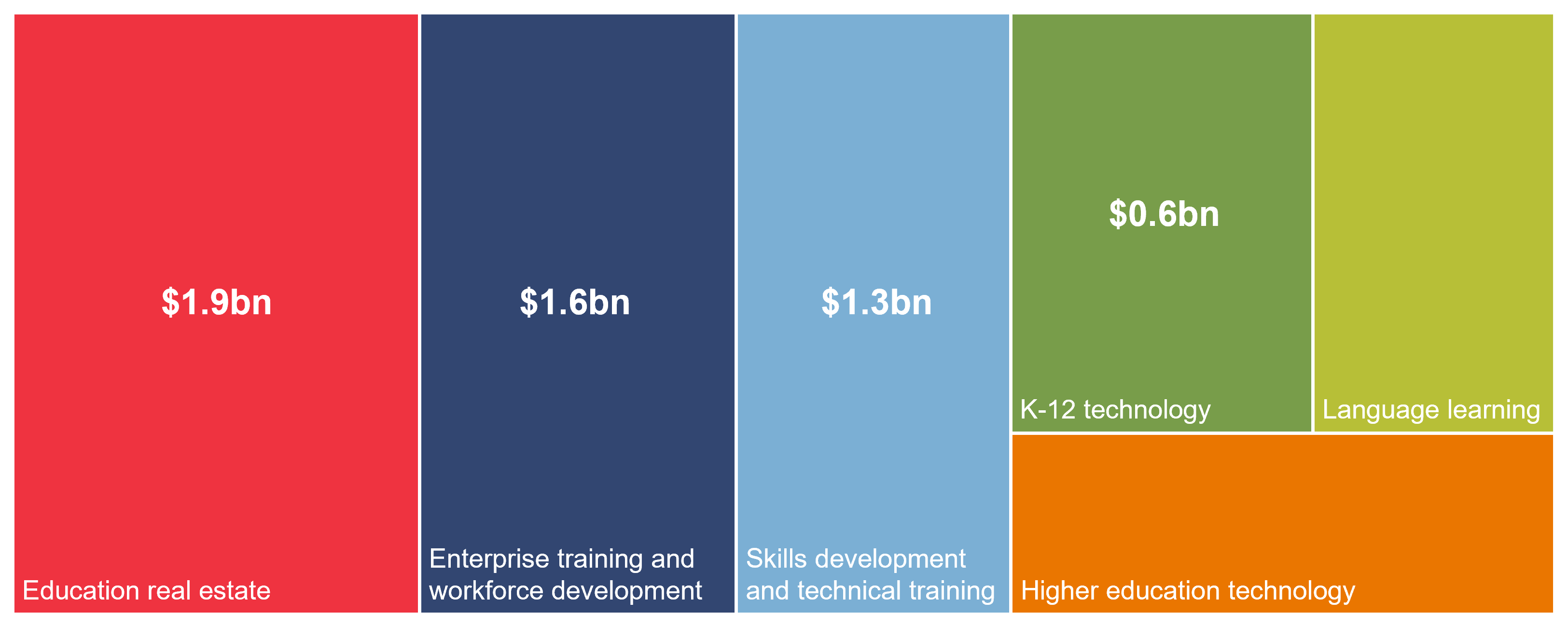

Education real estate has emerged as the dominant investment vertical as shown in Figure 5 below, with 77 deals worth $1.9bn between years 2020 and 2025. This segment encompasses mixed-use properties with educational components, including campus facilities, student housing, and educational infrastructure investments across diverse asset classes. The substantial real estate activity reflects institutional investors' appetite for stable, long-term assets with predictable rental income streams.

Figure 5: Education deal volume and value by vertical, 2020-2025

Note: Deal value ($bn) noted within the each vertical.

Source: Macfarlanes analysis; Preqin, Bloomberg; Data to 31 July 2025.

The workforce-focused segments demonstrate similarly compelling investment appeal, reflecting fundamental shifts in how skills development occurs. Enterprise training's relatively high proportion of PE deals stems from several potentially favourable long-term trends: the accelerating pace of workplace transformation, skills-based hiring practices becoming mainstream, and ongoing workforce development requirements driven by technological advancement.14 Unlike traditional education segments that may face budget constraints, enterprise training benefits from direct ROI visibility and corporate clients' willingness to pay for proven results.

The complementary skills development segment's strong performance also reflects global recognition that traditional educational institutions often cannot adapt quickly enough to address rapidly evolving workplace skill requirements15. Together, these infrastructure and workforce-oriented verticals captured 49.0% of total transactions and 59.1% of disclosed investment value over the past five years, potentially signalling investor confidence in education's physical assets and the growing market for continuous professional development.16

Resilience of traditional education

Moving beyond infrastructure and corporate-focused segments, traditional educational markets have shown notable investment appeal, with public budget pressures creating significant opportunities for private capital to drive technology-enabled efficiency solutions. K-12 technology's remarkable resilience reflects not only the permanent adoption of hybrid learning models but also institutional recognition that budget constraints necessitate more efficient operational approaches through technological integration.17 This consistency suggests investors recognise both the sector's capacity for sustained technology adoption and the compelling economics of solutions that reduce administrative costs whilst improving educational outcomes.

Between 2020 and 2025, higher education technology maintained steady investment levels with 31 deals, whilst emerging specialised segments like language learning (32 deals) and STEM education (24 deals) have benefitted from globalisation and technical skills demand respectively. Educational content and test preparation segments, with 13 deals and 11 deals respectively, round out a diversified investment landscape that spans the entire educational lifecycle.18

Venture capital as a dominant investment source

The deal structure preferences across education sector transactions reveal fundamental insights about market maturity and opportunities. Whilst the sector remains venture-dominated (79% of deals), these investments have evolved considerably. Average deal sizes fell from $37.1m in 2021 to $4.9m by 202319, potentially reflecting a preference for careful capital deployment in proven business models rather than large-scale platform experiments.

Conclusion

The education sector presents a compelling investment opportunity shaped by geographic concentration in an evolving market. Education's unique positioning as economic infrastructure underpins its investment appeal. The sector's role as a GDP multiplier, where each 1% increase in education expenditure corresponds to 21.3% GDP growth, distinguishes it from traditional service sectors through both direct returns and broader economic value creation. This dual nature provides defensive characteristics whilst creating substantial consolidation opportunities across a market projected to reach $8tn by 2030.

The post-pandemic normalisation, from 110 transactions in 2021 to 40 in 2024, alongside compressed average deal sizes signals market maturation beyond speculative investment toward disciplined, outcome-focused approaches. Whilst venture capital maintains its 79% share of transactions, the shift toward smaller, targeted investments may reflect increasing selectivity and focus on proven business models rather than experimental platforms.

The substantial venture capital activity observed across the education sector may create significant opportunities for PE investors in the medium term. As venture-backed education companies mature and demonstrate proven business models, they represent natural targets for PE buyouts seeking established platforms with validated market positions. This pipeline effect suggests that today's venture investment concentration could translate into enhanced deal flow for PE investors, particularly as early-stage education technology companies reach inflection points requiring growth capital and operational expertise that PE can provide. The sector's evolution from experimental digital learning platforms toward proven, outcome-focused business models aligns with PE's preference for companies with demonstrated revenue streams and clear paths to operational improvement.

This evolution may create opportunities for institutional investors who understand the sector's relationship-driven nature and regulatory complexity. The education market's fragmentation spans both geography and industry verticals, with education real estate facing property and planning requirements whilst education technology navigates data privacy and curriculum standards. This multi-dimensional complexity creates natural barriers to entry that may benefit established operators across multiple compliance environments.

In Part 2, we examine how investors navigate these regulatory complexities in the education sector through strategic pathways for value creation, specialised transaction execution approaches, and operational frameworks.

- Morgan Stanley (2023), Global Education’s $8Trillion Reboot.

- Macfarlanes analysis; Preqin; Bloomberg. Data to 31 July 2025.

- Morgan Stanely (2023), Global Education’s $8Trillion Reboot.

- Diakodimitriou, D., Tsioutsios, A., and Papageorgiou,T. (2025), "Education Expenditures and Growth: Is R&D the link?", Journal of Policy Modeling, Vol. 47.

- Psacharopoulos and Patrinos (2018), "Returns to investment in education: A decennial review of the global literature", Education Economics; Valero, A. (2021), "Education and economic growth", Centre for Economic Performance Discussion Paper No.1764, London School of Economics.

- Department for Digital, Culture, Media & Sport (DCMS) (2022). Quantifying the UK Data Skills Gap-Full Report.

- EQT (2024), Private Capital’s Role in Revolutionizing Global Education.

- Macfarlanes analysis; Preqin, Bloomberg; Data to 31 July 2025: total investment volume approximately $6.1 billion across disclosed dealvalues.

- Macfarlanes analysis; Preqin, Bloomberg; Data to 31 July 2025.

- Ibid, 2025.

- Ibid, 2025.

- Ibid, 2025.

- PE refers to private equity and RE refers to real estate.

- Macfarlanes analysis;Preqin, Bloomberg; Data to 31 July 2025.

- Macfarlanes analysis; Preqin; Bloomberg; Data to 31July 2025; Preqin Database Analysis, Key Investment Themes with Deal Counts -Corporate Learning: 60 deals.

- Department for Digital, Culture, Media & Sport(DCMS) (2022). Quantifying the UK Data Skills Gap-Full Report.

- Macfarlanes analysis; Preqin; Bloomberg; Data to 31 July 2025; Preqin Database Analysis.

- Dorbian, Iris (2024), Private equity goes back to school in education, Private Equity International.

- Macfarlanes analysis; Preqin; Bloomberg; Data to 31 July 2025; Preqin Database Analysis.

- Macfarlanes analysis;Preqin, Bloomberg; Data to 31 July 2025.